When it comes to coffee, there’s honestly too much I want to say—or rather, I’ve already said quite a lot. Three years ago, I started a small column dedicated to observing, tracking and analyzing China’s “coffee wars”—and that project is still very much ongoing today. 👇

Coffee is magical: it wakes you up, sharpens your mind, can even become addictive—and as long as you don’t overdo it, it’s actually good for your health. It’s similar to tea in terms of function, yet completely different in flavor; its energizing effect is almost instantaneous, more intense physiologically than tea, and naturally fits the fast pace of urban life.

On an emotional or culture-level, it represents a kind of Western lifestyle that is quality, free, and cool. That’s probably coffee’s innate advantage in China and across much of Asia: it has a built-in appeal for young people here.

In the past few years, thanks to mainstream media coverage, the outside world’s impression of Chinese coffee has long been stuck on the “Luckin vs. Starbucks” battle. This shallow understanding stems partly from entrenched biases about the Chinese market. On the other hand, much of the content out there in the market — mine included — still looks at coffee mainly from the consumer side, and lacks an industry perspective. That inevitably leaves readers with a somewhat one‑sided understanding of the coffee market.

Some have blamed Starbucks’ troubles in China solely on “macro headwinds + a price war,” but the reality is more complex — how does a single brand like Luckin outperform a giant like Starbucks? It’s the rise of China’s coffee industry that makes the once-dominant Starbucks look mediocre here. I’ve discussed this in earlier articles — feel free to refer back to them below. 👇

So, this time, I want to do something slightly different — Let’s step away, for a moment, from the stage of “storefront or consumer perspective” and move the camera a layer deeper:

Where exactly do these coffees come from? Who is actually supplying the resources behind the cup in Chinese consumer's hand?

In fact, the coffee value chain is far more complex than most people imagine—from farming, picking and processing, to roasting, logistics, and finally landing in cafés or in consumers’ hands. Beyond that, there are futures markets, industry associations, trade shows, competitions, and grassroots communities all working together to empower and reshape this industry.

Today, I’ll start from one of the least-talked-about areas in the mainstream media—the origin of coffee: Green Beans (coffee before roasting) — and use that as an entry point to keep piecing together the puzzle of “China’s coffee world.”

If you found value here, please share this article and consider a paid subscription — your support keeps this going. 🌟

I’ve mentioned many times before — the Chinese market is unique in a very specific way—you may recall this: China is probably one of few places in the world that simultaneously has ultra-large-scale coffee consumption (a market worth hundreds of billions of RMB) + significant-scale coffee cultivation (currently ranked 14th globally). This combination almost guarantees that the brands, habits, and trends that emerge on this land will look different from anywhere else.

On one hand, it has given birth to massive coffee chains that drive consumption—Luckin, Manner, and now players that have crossed over into coffee, like Mixue and Gu Ming. On the other hand, this demand has in turn fed back into local production.

“Yunnan 云南” coffee now accounts for over 35% of China’s total coffee sales. And perhaps unexpectedly, “Hainan 海南” is also a coffee-growing region, though very small, contributing about 2% of domestic coffee bean output.

Taken together, these numbers make one thing very clear: the vast majority of green coffee consumed in China still comes from overseas rather than domestic production.

Notably, China is now a major importer of green coffee beans, bringing in around 200,000 tons each year, with 13.5 % yoy growth rate in 2025. The total consumption of green coffee here already ranks among the top ten in the world, according to a report by Science and Technology Daily.

Although green coffee beans have many physical attributes, the simplest and most intuitive way to classify them is by origin. So in this article, I’m not going to dwell too much on grand narratives. Instead, I want to start from a more micro perspective—the coffee-growing origins that are popular in China—to show how these beans are actually shaping the market here 👇

Let’s start at my home (China): Yunnan & Hainan

Yunnan: between being “looked down on” and “looked forward to”

First, some context,

The coffee market can be roughly divided into commercial coffee and specialty coffee: Commercial coffee: lower-quality beans that only need to satisfy the basic function of “keeping you awake.” Specialty coffee: higher-quality beans that not only energize you, but also offer flavor, terroir stories, rarity, and other variables that support a more “premium” experience.

This is also why, when I previously categorized cafés, I personally split them into three types: Chains (commercial coffee–led) ; Specialty chains (specialty coffee–led) ; Independent cafés (specialty + distinct positioning or personality — otherwise hard to survive)

Fundamentally, this is a basic segmentation along the axis of commercial vs. specialty coffee. With this in mind, it becomes much easier to understand how different beans are used and valued in the market.

For a long time, Yunnan’s overall bean quality lagged behind traditional origins, so most of its output went into: Instant coffee products or some inferior roasted blends. The proportion that could actually enter the real specialty market used to be consistently below 5%. But as the specialty segment has boomed in China in recent years, in 2024, this number is up to 30%!!!!!!!

However, some specialty varieties—Typica 铁皮卡, Caturra 卡杜拉, Geisha 瑰夏, SL28, Bourbon 波旁 etc.—are still planted in much smaller volumes, and experience is limited, though acreage has been expanding in recent years. Now, most of the coffee planted in Yunnan is still Catimor 卡迪姆, a variety that is easy to grow but lower in cup quality.

Catimor itself is genetically predisposed to certain flavor notes—woody, smoky. In professional coffee circles, this isn’t automatically a “defect.” But for Chinese consumers—especially when Catimor is processed and roasted poorly—pulling it out as a single-origin and asking people to drink it straight is often a recipe for total rejection.

On top of that, compared with other origins, labor costs in Yunnan are high, which is another reason why Yunnan specialty beans have long been stuck in an awkward position:

In short: not that tasty, and not that cheap.

Just look at these screenshots from XHS: on the left, a user complains that Yunnan coffee tastes flat and uninteresting; on the right, a barista from a well-known café bluntly says that Yunnan beans are both not tasty and expensive—so most coffee shops simply choose not to use them 👇

Worse still, in order to compete with international beans, some Yunnan producers resorted to shortcuts in processing: Artificial flavoring in “fermentation” Poor technique leading to unnatural, overly perfumed flavors — so called Artificial flavored beans 香精豆; Trying to aggressively manipulate flavor to mask inherent weaknesses of the beans; Even scandals where Catimor was sold as higher-value varieties like Typica. All of this understandably angered both consumers and professionals. Confidence and trust in “Yunnan specialty coffee” went through a real low point.

To adapt to changing market demands and rebuild trust, the Yunnan government and industry players have been pushing hard on multiple fronts in recent years: Upgrading farming and processing techniques;Investing in infrastructure;Attracting more talent into Yunnan’s coffee-growing sector;Introducing new varieties;Tightening market management and improving transparency and etc…

Under these changes, more and more Yunnan coffees have clearly improved in quality.

For example: The harsh, unpleasant finish often associated with Catimor has become less pronounced in many lots. Some lots of varieties—like “Sarchimor” (萨琪姆) — have shown surprisingly Ethiopia-like profiles, with faintly clean acidity and sweetness. Certain estates and batches have even delivered flavor experiences strong enough to stand shoulder-to-shoulder with world-class coffees.

My cupping experience makes one thing very clear: Yunnan is undergoing a drastic transformation. This year’s slots are a completely different animal compared with those from even two years ago. The market just hasn’t fully caught up yet—it needs some time to react.

However, we shouldn’t celebrate too early. We still have to admit that, compared with origins like Ethiopia and Panama, Yunnan as a whole still has a big gap: quality is unstable, differences between batches and farms are huge, and corner‑cutting and mislabeling still occur.

So I don’t want—and refuse—to irresponsibly “canonize” any particular Yunnan variety or estate here. This isn’t Ethiopia or Panama; you can’t assume consistency easily. A batch I find excellent might be followed by another batch that you find mediocre or worse. For a region or estate to truly get things right, it often takes many years, if not decades, of iteration and proof.

Don’t get me wrong—I’m not trying to pour cold water on Yunnan coffee. Its progress is obvious to anyone who’s been paying attention: from disappointment and anger, to sympathy (“what a shame”), to finally those moments of surprise you get after stubbornly “sifting the sea with a spoon.” That full emotional arc is exactly what keeps people who care about Yunnan coffee curious and willing to keep trying — Here, no one genuinely wants to see it fail.

If you have professional skills, long-term ambition, or capital in this space, Yunnan is absolutely worth a long-term investment. Personally, I’m more inclined to look at it on a 5–10 year horizon rather than one or two. I do believe that one day, it will deliver a real surprise to the world.

Hainan: small and bitter, carrying “caffeine and cost” on its back

What might surprise you is that China has another coffee origin: Hainan.

The elevation there is low, and the climate is hot and humid—conditions that are suitable for growing robusta. The issue is that these beans tend to be “too intense” in aroma—put simply, they’re very bitter, often carry rubbery notes, and are very high in caffeine. For most consumers, that’s hard to enjoy on its own.

So for now, their value is mostly realized in: Instant coffee products and as a supporting component in certain blends.

The role is similar to some of the more basic-quality Yunnan beans: They take on the “bitter + strong caffeine + cost reduction” job that no one sees, but the market needs.

Of course, top-grade robusta can compete with arabica in cup quality. But Hainan’s overall output is so small that even if there are excellent lots, their market impact is still minimal. So I won’t go deeper into that here today.

Halftime recap: a rough but real “map of China’s green beans”

If we roughly divide the sources of green beans in China by function, the picture looks something like this:

Yunnan: Transitioning from “cheap base + instant material” toward “promising but unstable specialty option.” On one side, dismissed as “overpriced and underwhelming”; on the other, burdened with the hope that it might one day represent China on the specialty stage.

Hainan: Small-origin, small but bitter—mainly responsible for “bitterness and caffeine” in instant and deep-roast blends.

Alright, let’s put the domestic part on pause for now.

As mentioned earlier, imported green beans already account for a larger share of the market than locally grown ones—and in terms of both scale and overall quality, they are still ahead of domestic beans.

According to China’s 2024 customs data, the main sources of imported green coffee were Brazil in first place, followed by Colombia, Vietnam, Ethiopia, Indonesia and Uganda. By 2025, however, the ranking had shifted: Ethiopia moved into first place, followed by Vietnam, Uganda, Brazil, Indonesia and Colombia.

Among them, the standout is Ethiopia: in 2024 it was still in fourth place, but by 2025 it had jumped to first, with imports increasing by a staggering 124%.

Let me put it in this way — at least for the moment, it’s these imported green coffees that are truly working behind the scenes to shape Chinese consumers’ taste preferences. But how? 👇

PS: In addition to these high‑volume suppliers (Ethiopia, Vietnam, Uganda, Brazil, Indonesia, Colombia), I will also talk about Panama — its import volume is small, but it’s the flagship origin in the high‑end coffee segment

Imported Beans:

Ethiopia: China’s Best‑Selling and Most Influential Origin Today

Ethiopian green coffee holds a special position in the Chinese market for several reasons.

First, policy: China offers tariff exemptions to Ethiopian imports (and is phasing in zero-tariff treatment for more African countries), which gives Ethiopian coffee a natural price advantage.

Second, flavor: Ethiopian beans usually bring - Distinct florals and fruity aromatics - Bright but approachable acidity - Smooth, layered mouthfeel — lower‑grade lots often go into blends, while higher‑grade ones are typically used as single‑origin pour‑overs.

All of which align very well with the preferences of today’s mainstream urban coffee drinkers in China. So while few professionals will say this outright in “official” contexts, my personal view is — Ethiopia has become the de facto benchmark for everyday pour-over coffee. In simple terms: If your beans are more expensive than Ethiopian, you’d better offer something truly unique.

Let’s zoom in.

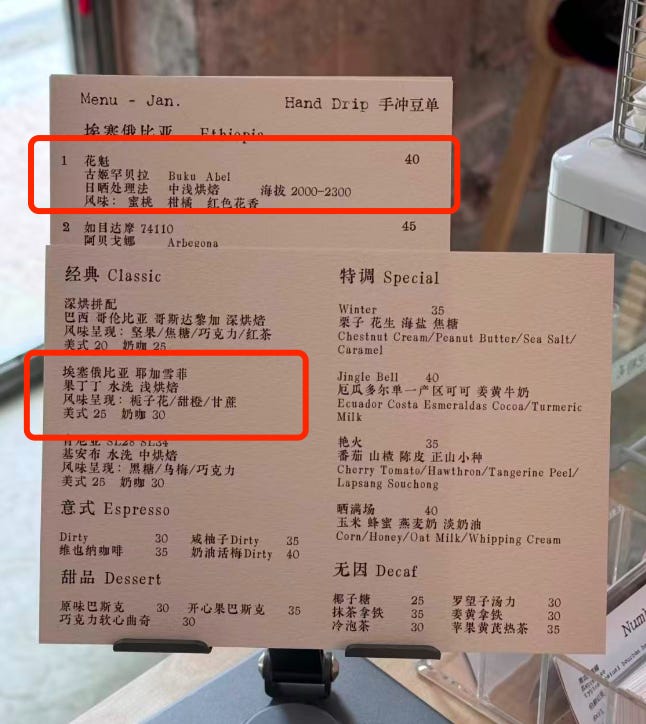

One major popular category is beans from Yirgacheffe region: Under light roasting, their jasmine aromatics are unforgettable.

Another category is, unsurprisingly, Gesha: whatever Gesha or Geisha sells, even most consumers can not really tell the difference. Well — Ethiopian Gesha in particular tend to have very intense florals and fruitiness, bright acidity, and outstanding cleanliness. It was one of the coffees that first introduced Chinese consumers to Gesha after Panama’s Geisha.

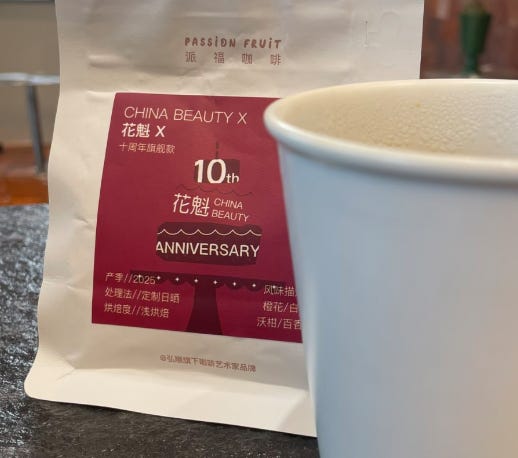

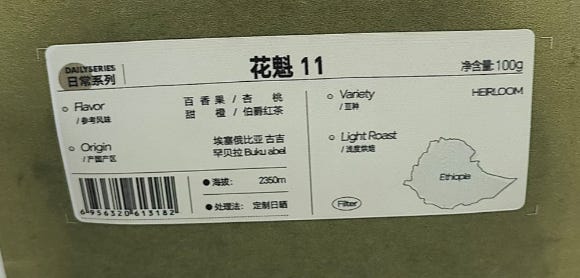

Notably, there’s an interesting coffee bean in the Chinese market: Oiran (花魁, which some people simply call “China Beauty”) 👇

The bean itself is a natural-process coffee beans from the Hambela, Buku Abel Station, selected by Ethiopia’s DW Coffee Export back in 2017. It won the Taste of Harvest (TOH) competition and was brought into China by a trader in BJ, where it was rebranded as “Oiran” (literally “queen of flowers 花中之王” in Chinese).

In fact, this name doesn’t align with what it’s called abroad. Outside China, it’s usually just called Hambela.

Let me slip in an interesting story here — you’ll notice that “Oiran” on the market keeps being renamed with each new import batch: from Oiran 1.0, 2.0… all the way up to the latest 11.0.

And there’s no 10.0 in between. Why?

Because some domestic green coffee traders wanted to “pay tribute” to Apple 🍎 and copy the iPhone naming strategy, so the 10th-generation coffee was simply called Oiran X. 😂

Admittedly — just like “Geisha” and “Yirgacheffe,” the Chinese name “Oiran” is pure genius: Simple and memorable; Expresses exactly what’s special about the coffee—intense florals and a tea-like structure; Carries rich cultural imagery. That naming stroke alone helped this origin dominate Chinese specialty coffee menus for years — its market recognition level is now on par with Geisha and Yirgacheffe.

Recently, the way coffee beans are named and marketed has been quietly changing. Over the past two years in China, there’s been a growing focus on:

Named producers (like ALO, ETLO, etc.), and

Specific varieties (such as 74158, 74100, etc.).

These details now often appear as explicit selling points on the menus of serious specialty cafés — and this isn’t just true for Ethiopia; other origins are following the same pattern.

On one level, you can read it as increased transparency on beans supply chain. On another, a lot of it is being pushed from the marketing side — The logic is simple: if you keep selling the same old “country / processing / flavor” formula forever, people are eventually going to get bored.

Indonesia: the “dark roast king”

Indonesia’s flagship in China is Mandheling 曼特宁.(I am not taking abt Robusta here)

In central and southern China, Mandheling is no longer popular as a single-origin espresso or pour-over; more precisely, it had its moment, but has gradually been replaced by more floral and fruity coffees. (Of course, as a component in blends, Mandheling is still one of the most widely used and enduring recipes.)

Why?

To me, Mandheling does have some redeeming good features — cocoa, caramel and deeper body. But it also comes with herbal and woody notes, and often bitterness. Even with deep roasting to mask some defects, it can still carry off-flavors — herbal medicine vibes, muddiness—that many Chinese customers find off-putting.

Of course, even many “consensus-trained” experts are reluctant to admit something — Thoughtful deep roasting + precise brewing = can unlock a side of dark roasts most people never see: stunning sweetness and surprisingly clean cups. It’s just that very few barista + roasters can actually execute this consistently. Anyone who has really experienced good dark roasts will know what I mean.

One more interesting thing I’ve noticed about Mandheling is a kind of geographic–cultural wrinkle👇

Perhaps because northern Chinese consumers are used to stronger alcohol and bolder flavors, or maybe because the north has been more influenced by Japanese dark‑roast culture, cities like Beijing show a much higher tolerance dark roasts and straight black coffees and Mandheling is actually a star product in many cafés there. This stands in clear contrast to the south, where people generally prefer brighter, lighter‑roasted beans.

Vietnam & Uganda: the invisible backbone of instant and espresso blends

Vietnam and Uganda share a key trait: both are robusta powerhouses. In China, their main roles are: Raw material for instant coffee and Base layer in espresso blends

They contribute: Bitterness; Crema and body; And help keep overall costs under control. You rarely see “Vietnam estate X” or “Uganda micro-lot Y” on café menus. but on procurement sheets in factories and roasteries, they’re anything but invisible.

In many ways, they’re the uncredited workhorses of China’s coffee industrial complex.

Brazil: the crucial chassis

Brazil is probably the most “invisible yet crucial” origin in today’s Chinese coffee cups.

Its role is simple - Flavor-wise: nutty, chocolaty, caramelly, full bodied; Quality-wise: solid and very consistent — Operationally: ideal for large-scale, reliable sourcing

Key facts: Luckin buys about 60% of all Brazilian coffee imported into China. Many premium espresso blends also choose Brazilian beans as their base to ensure intensity and consistency.

Colombia: a love–hate relationship

Colombia is a textbook “polarizing” origin:

On one side, it produces a number of truly high-quality Geisha, Bourbon, and other great varieties.

On the other, it might the one of the most aggressive origins in experimenting with special processing in the world.

Unfortunately, Chinese consumers are particularly sensitive to this now, partly because in Yunnan, as I just mentioned, we went through a whole phase where “artificial flavored” and “over-processed” beans were used to mask poor raw material —so for many people, “special processing = cheating” became a default mental shortcut. So many cafés now treat “no artificial flavored beans” as a moral bottom line. This emotional backlash has hit good Yunan and Colombian coffees as well.

I can’t say this is the only reason, but the outcome is clear: Colombia’s green bean imports into China have been on a clear downward trend last year, and that lines up closely with what I’ve been observing in terms of changing consumer preferences on the ground.

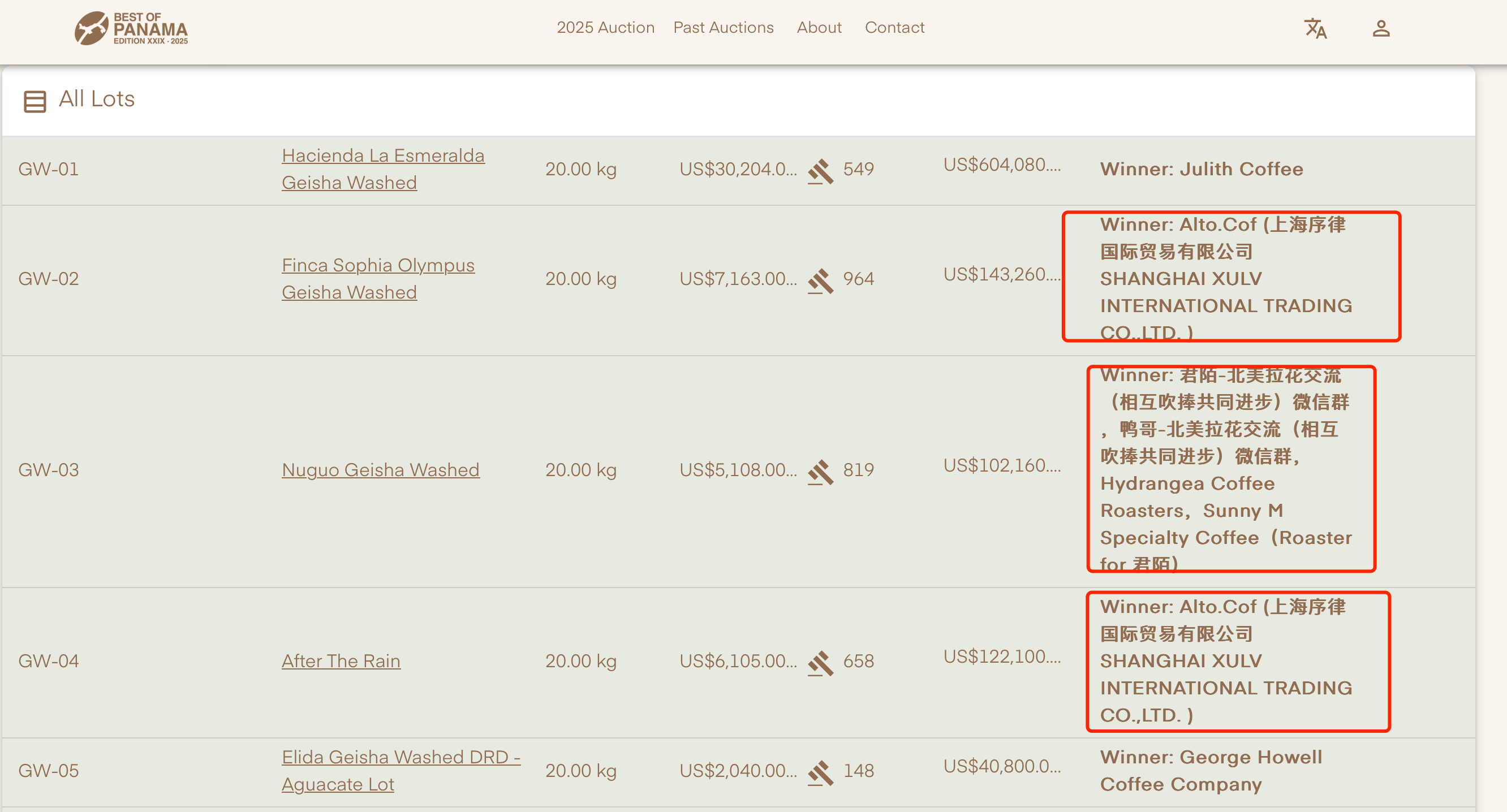

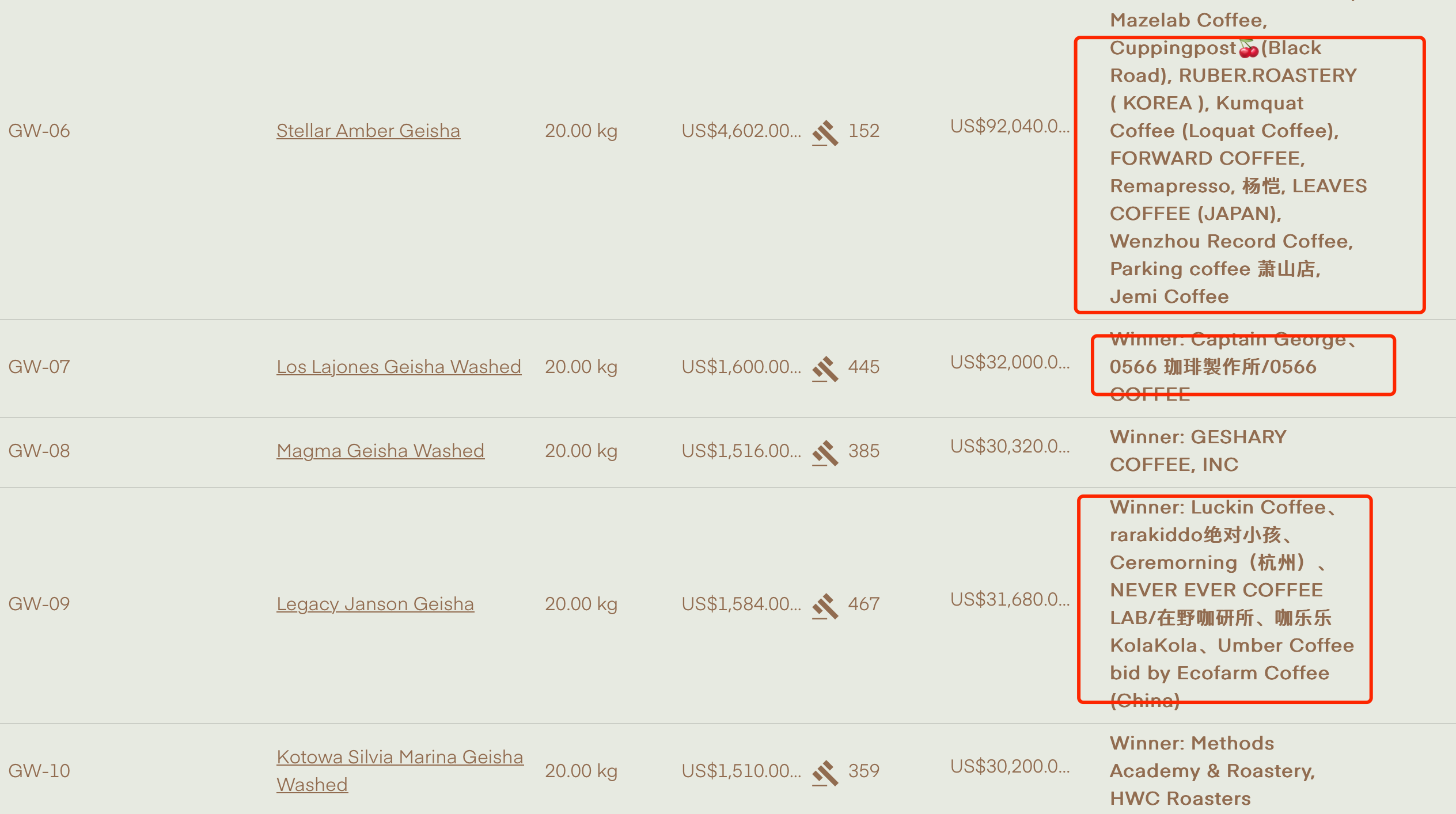

Panama: in the high-end game, China is no longer just a spectator

When it comes to high-end coffee beans and “street cred,” Panama is almost impossible to avoid.

In the minds of most serious coffee lovers, “Panama Geisha” is no longer just an origin + variety label. It’s a whole package of symbols: Exquisite florals; Complex fruit acidity ; Layered sweetness and tea-like structure; Very high cupping scores; And, increasingly, absurd auction prices.

What many people may not realize is this:

In recent years, a large share of those record-breaking auction lots from Panama—the ones that make global headlines — have been bought by Chinese buyers.

Here is a selection of buyer information from the official website of the 2025 Panama coffee auction 👇

This sends two strong signals:

1. China is no longer a follower, but an active player in the high-end pricing game.

When you’re willing to pay the highest prices in the world for a coffee, you’re not just buying beans — you’re participating in defining - What counts as “top-tier flavor” in the coming years — Which processing methods and origins others will try to emulate

2. Panama’s industry now has to take “Chinese taste” seriously.

When one of your biggest buyers is from China, it becomes inevitable that: Chinese judges appear on juries and more professionals show up at origin.

This isn’t token representation; it’s about building Chinese consumer’s preferences directly into the auction feedback loop - impact the whole supply chain eventually.

In the end…

To wrap this up, if I had to force everything into one sentence, the current “green bean battlefield” in China roughly looks like this — Imported beans are supporting the fast-growing coffee consumption civilization we live in today; Domestic beans is quietly laying the groundwork for a future that hasn’t fully arrived yet.

No doubt, the story of green beans is far from over—what I’ve done here is only to open up the map a little. A single article can’t possibly cover every origin, nor can it do justice to all the detailed trends. In the future, I’ll probably write more pieces that dive into specific subtopics on the bean side.

Needless to say, a green bean on its own can’t go straight into your cup—it’s just raw material. To become good coffee it must pass through a whole series of steps, as discussed. The next article in this coffee series—though not finalized—will most likely focus on coffee roasting in China, a crucial link between the bean and the bar.

If this interests you, please consider sharing this piece and subscribing. Thank you.

Before you go, I would suggest — when you next reach for a “good cup of coffee,” maybe consider giving Yunnan specialty beans a shot. That seemingly insignificant cup can translate into real income for farmers, and more incentive to plant and improve better coffee. And whether you end up liking it or not, your feedback is still valuable—it becomes part of the reference that helps them get better.

I had lived in Beijing about ten years ago, and I still remeber the amazement I felt, witnessing both the rapid expansion if Starbucks and emergence of Luckin. Sometimes I wondered how the coffee scene in China has changed since I left, and your article on supply side is very interesting. As a consumer outside of China, ensuring process transparency might be the key in buying quality beans.

Maybe because I spent time in Hainan early on, coffee there was never a surprise to me! I've always appreciated how ubiquitous coffee was in China, being redefined every day. Starbucks is still the best "3rd place", while others get the delivery convenience model, or add coffee to what is essentially, other desserts. It's all good.

I had lived in Beijing about ten years ago, and I still remeber the amazement I felt, witnessing both the rapid expansion if Starbucks and emergence of Luckin. Sometimes I wondered how the coffee scene in China has changed since I left, and your article on supply side is very interesting. As a consumer outside of China, ensuring process transparency might be the key in buying quality beans.

Maybe because I spent time in Hainan early on, coffee there was never a surprise to me! I've always appreciated how ubiquitous coffee was in China, being redefined every day. Starbucks is still the best "3rd place", while others get the delivery convenience model, or add coffee to what is essentially, other desserts. It's all good.